Life Insurance That Helps While You’re Alive: Understanding Living Benefits

Most people think of life insurance as something that helps their family after they pass away. But some life insurance policies can also provide support while you are still alive. These policies include living benefits, which can offer financial help during difficult times, such as a serious illness or injury. Living benefits may help cover medical expenses, replace lost income, or assist with unexpected costs.

This guide explains what living benefits are, how they work, and what to consider when choosing a life insurance policy.

What Are Living Benefits in Life Insurance?

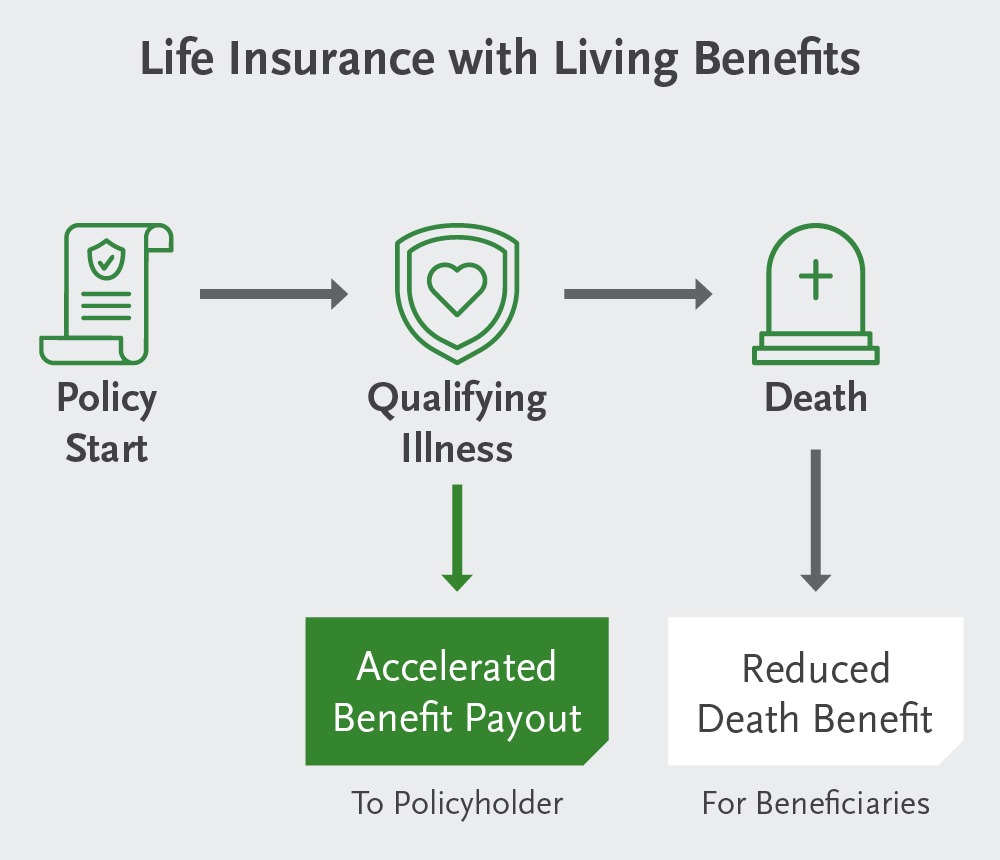

Living benefits are sometimes supplemental and optional features in a life insurance policy that can help support you financially during major health or life events. Think of them as an advance on your policy’s payout, though any amount accessed. Any amount accessed through living benefits is deducted from the benefit your loved ones would receive later called the death benefit. Under insurance model regulations, living benefits—also called accelerated benefits riders—are amounts potentially paid from a life insurance policy to the policyowner during the insured’s lifetime after a qualifying event. An amount paid is deducted from the policy’s death benefit.

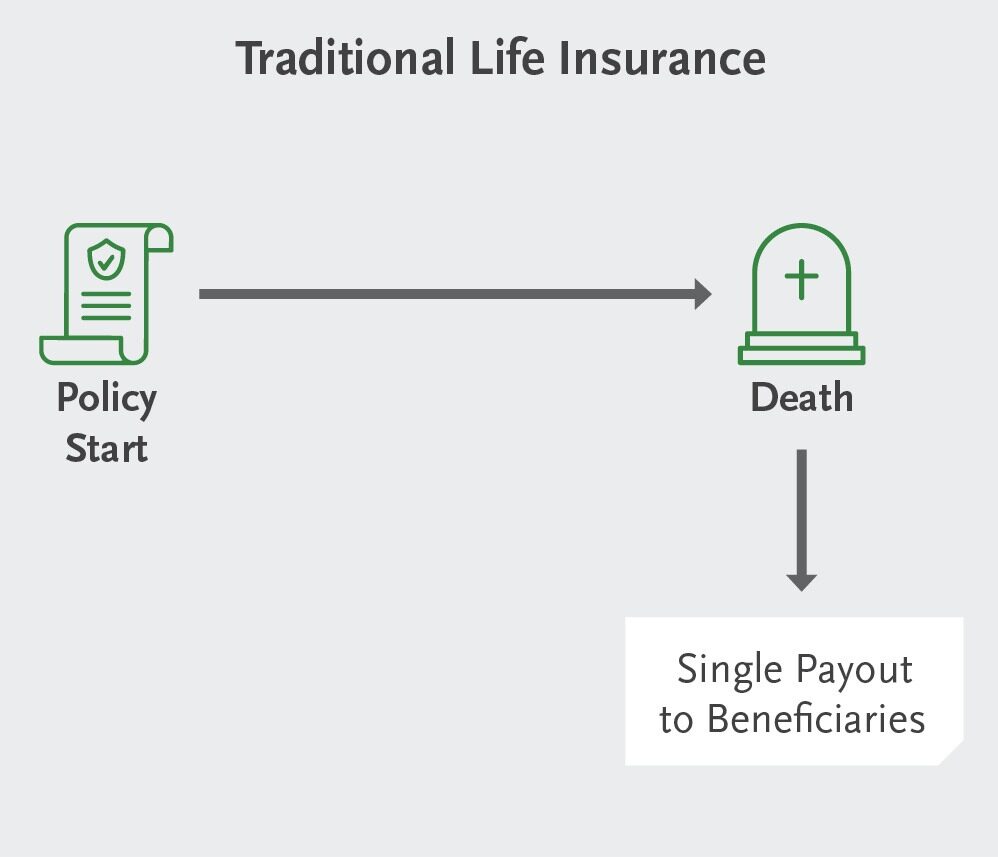

Life Insurance: Traditional vs. Living Benefits Comparison

Common Types of Living Benefits

There are two main ways you can access living benefits in life insurance policies: Accelerated Benefit Riders (ABRs) and the potential policy cash value.

ABRs for Qualifying Illnesses

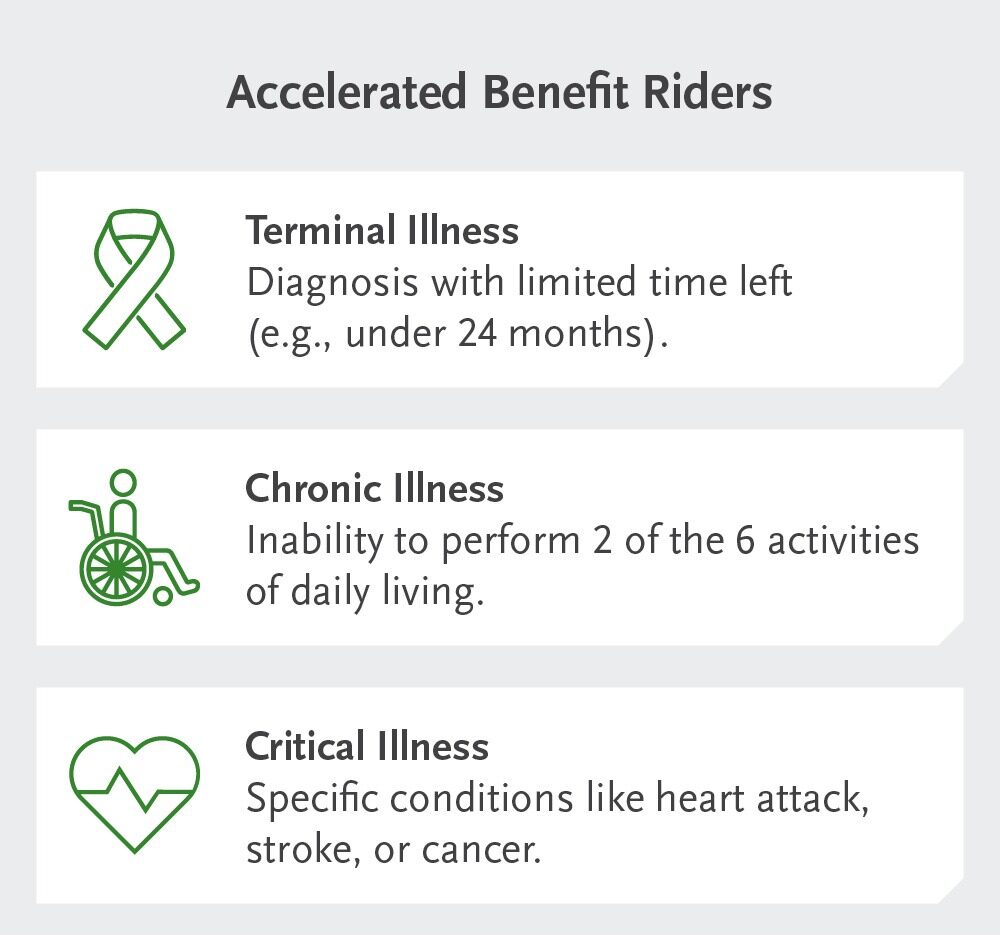

Accelerated Benefit Riders (ABRs) are one of the most common types of living benefits. They may be included in both term and permanent life insurance policies. Some ABRs are part of the base policy premium, while others may require an additional charge.

Common ABRs include:

- Terminal Illness Rider: May allow access to part of your death benefit if you are diagnosed with a qualifying terminal illness.

- Chronic Illness Rider: May provide benefits if a qualifying chronic illness event occurs, subject to policy definitions. It may be available if a medical professional confirms you cannot perform at least two of the six activities of daily living – like bathing, dressing, or eating – without help. The six Activities of Daily Living (ADLs) generally include bathing, dressing, eating, toileting, transferring (moving in and out of a bed or chair), and continence, as defined in the policy and applicable state rules.

- Critical Illness Rider: May allow access to a portion of your death benefit if a qualifying critical illness occurs.

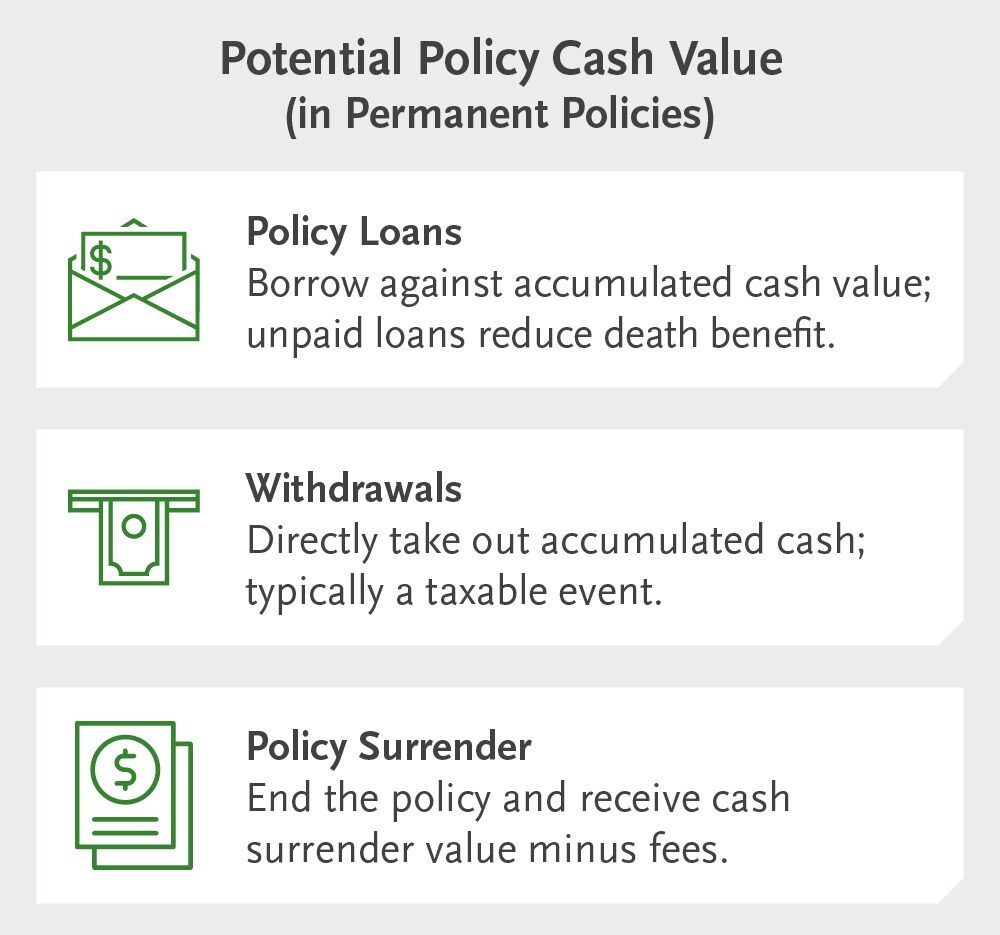

Potential Policy Cash Value Permanent Life Insurance

Permanent life insurance policies, such as Whole Life or Indexed Universal Life (IUL), may build cash value over time. Policyholders may access this value through policy loans or withdrawals. Loans and withdrawals may reduce both cash value and death benefit and can cause policy lapse if not managed properly.

Cash value access is different from living benefits because it does not require a qualifying health event, but loans or withdrawals will reduce policy values and may cause a policy to lapse if not managed properly.

Ways to potentially access cash value include:

- Policy Loans: Borrow against accumulated cash value; unpaid loans reduce the death benefit.

- Withdrawals: Take money directly from the cash value for a large purchase or unexpected expense.

- Policy Surrender: End the policy and receive the net surrender value, minus applicable charges.

For many people, the potential to access the policy’s cash value can be a flexible financial tool. It’s can help with emergencies, possibly supplement retirement income, or even a down payment on a home.

Real-Life Situations Where Living Benefits Can Help

Living benefits can make a meaningful difference for families facing unexpected challenges.

Examples include:

- Covering bills while taking time off work to care for a loved one.

- Helping maintain financial stability when a primary earner stops working due to illness.

- Reducing financial stress so you can focus on recovery.

- Providing support after diagnoses such as cancer or serious injury.

- Provide financial support after a diagnosis like cancer or a serious injury.

Learn more from Lita’s Living Benefits story

Life is unpredictable, but your financial security doesn’t have to be. Talk to a financial professional to learn how a life insurance policy with living benefits may fit into your strategy.

Frequently Asked Questions

Do living benefits cost extra?

Some living benefits are included at no extra cost; specialized riders may require additional premiums.

If I use my living benefits, what happens to the death benefit?

Any amount used is deducted from the policy’s final payout.

Are living benefits taxable?

They may be, depending on your situation. Tax implications vary, and benefits may also affect eligibility for public assistance programs. Consult a tax advisor.

How is cash value different from living benefits?

Living benefits are tied to qualifying health events. The life insurance policy’s potential cash value may be accessed in some permanent life insurance policies.

National Life Group

The National Life Media Team produces educational content focused on financial literacy, insurance, retirement, and long-term financial preparedness, helping individuals and families better understand complex financial concepts.

TC8736547(0226)3