Women earn 78 cents to every dollar that men earn, according to the U. S. Department of Labor. That’s 23% less than their male counterparts. On top of that, the 2010 U.S. Census reports that 42% of all women lack financial security.

Susan Jennings is passionate about changing those statistics. Susan is Senior Legal Counsel for National Life Group and Executive Committee Member of the Indexed Annuity Leadership Council. She has been with National Life for 29 years. Since her days in law school, she has been an advocate for women’s professional development and has been a proponent of breaking down gender stereotypes.

I had the pleasure of sitting down with Susan to get a sneak peek of the topics that will be covered during the panel discussion, The State of American Retirement: Navigating the Gender Imbalance. On October 15. Susan will join other influential financial and retirement experts in Washington D.C. to discuss ways to bridge retirement’s gender disparity so that all women are aware of how to prepare for a secure retirement.

What are some of the key gender imbalances related to financial planning and retirement?

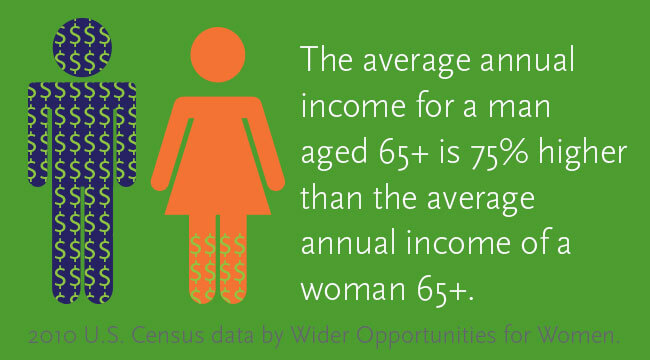

Overall, women have saved far less for retirement than their male counterparts, and these same women are likely to live longer and actually need more to provide for their retirement needs. As the American population ages, we find that more and more women who had lived comfortable lives are entering poverty or near poverty in their retirement years.

Why is this the case?

Generally, women have less awareness about financial topics and defer financial decisions and responsibility to their spouse. This is particularly true in households where men are the primary breadwinner, but even in families where the woman is the primary wage earner, financial decisions, particularly decisions related to long-term retirement planning are often left to men or are left unaddressed completely. In many cases single-women, particularly single-mothers, feel the pressures of meeting daily expenses and don’t prioritize the importance of long-term saving. In fact, often times during divorce settlements women are primarily concerned with ensuring immediate care of the family and don’t even address the issue of dividing retirement assets.

It sounds like a large and significant problem, what can be done to change the situation?

It is a significant problem, and that is why we are convening the panel discussion to address the situation. We want women to be aware of the choices and options that are available to them and we need our legislators to know that retirement plans should not just allow employees to accumulate funds for retirement, but should also provide a determinable amount of income for the rest of their lives.

What are some of the things women can do today to shift the tide?

Well, one of the things that we can all do is make financial literacy and long-term saving a part of the dialogue with all women beginning with young girls. It is never too early to start talking about planning and saving for the future and it is never too soon to start learning about the tools that are available to make saving for the future possible. And I’m not talking about reading the Financial Times and Wall Street Journal, I am talking about using the many, many resources that are available on the Internet that are delivered in simple straight-forward language that are easy to understand and digest.

There are so many great blogs available for women to follow, that offer financial information from every perspective—be that of a young professional just starting out, to a stay-at-home mom, to a working mom trying to juggle family and career, to a single parent trying to live and save on one income. There are stories that every woman can relate to and identify with, and this is the type of conversation and information that needs to be shared so that every woman can understand that saving and providing for her future is and should be within her own power.

Additionally, there are online calculators and resources that can help people budget and determine how much they need to save in order to meet their retirement goals.

If you could provide women with one piece of advice related to retirement planning and saving, what would it be?

The single best piece of advice related to retirement saving is the same for everyone, whether women or not: save as much as you can, as early as you can. Start saving from the time that you get your first paying job—even if that is in your teenage years, it will form the habit of saving for the longer term and even small amounts can turn into something substantial over time. Specifically for women, the amounts they can save early in their career will really make a difference if they decide to take time out of the workforce in order to care for children or family members.

Additionally I would advise women to be aware of their risk tolerance. The prevailing message out there is that mutual funds and stock market based investments are the best way to accumulate long-term growth. Women have inherent needs for security and stability, and need to be mindful that the aggressive ebb and flow of the market may not be the most palatable way to build their nest egg.

There are many other conservative savings and investment options to choose from, including fixed indexed annuities, which can provide upside interest potential in a positive interest rate environment but still provide protection of principal and guarantees when the markets are negative or volatile.

Join Susan Jennings at The State of American Retirement: Navigating the Gender Imbalance.

Securities can be offered solely be representatives registered to offer such products through a broker/dealer. Financial planning and investment advisory services can be offered by investment adviser representatives through a registered investment adviser.

An Indexed Annuity (IA) is usually a fixed annuity whose interest is determined, at least in part, by the performance of a specified index of the market. Unlike traditional fixed annuities, the policyowner may receive zero interest for a single period on a specific premium payment if the index performs poorly. However, with most designs, the premiums are protected and guaranteed to grow over time, and the owner of an equity indexed annuity may experience better interest crediting than a traditional fixed annuity during periods when the market performs well. Indexed annuities do not directly participate in any stock or equity investments. An investment cannot be made directly into an index. Most IAs permit owners to participate in only a stated percentage of an increase in an index, and also impose a “cap rate” that represents the maximum annual account value percentage increase allowed to contract owners. Because they are meant for long-term accumulation, most annuities have surrender charges that are assessed during the early years of the contract if the contract owner surrenders the annuity. In addition, withdrawals prior to age 59 ½ may be subject to a 10% Federal Tax Penalty. The guarantees of annuity contracts are contingent on the claims-paying ability of the issuing insurance company. All withdrawals made from annuities with pre-tax contributions are taxed as ordinary income. All withdrawals from an annuity purchased with non-qualified monies are taxable as ordinary income only to the extent there is a gain in the policy. This is not a solicitation of any specific annuity contract.

TC87097(1015)1